The Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest Act, 2002 (also known as the SARFAESI Act) is an Indian law. It allows banks and other financial institution to auction residential or commercial properties (of Defaulter) to recover loans. The first asset reconstruction company (ARC) of India, ARCIL, was set up under this act. Source Wiki.

The SARFAESI Act was passed on December 17, 2002, in order to lay down processes to help Indian lenders recover their dues quickly. The SARFAESI Act essentially empowers banks and other financial institutions to directly auction residential or commercial properties that have been pledged with them to recover loans from borrowers. Before this Act took effect, financial institutions had to take recourse to civil suits in the courts to recover their dues, which is a lengthy and time-consuming process. Source thehindubusinessline.com

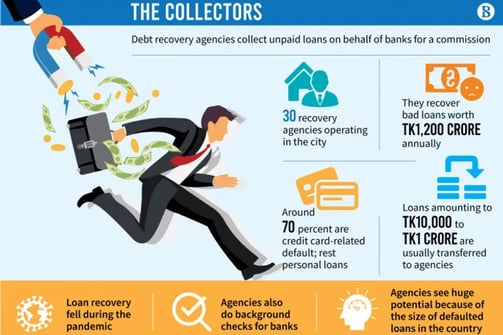

When a bank is unable to recover loans from a customer, it hires a third-party debt collection agency to help.

Good Article from www.tbsnews.net Click To Access

Picture from tbsnews.net News Article

The Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI) empowers Banks / Financial Institutions to recover their non-performing assets without the intervention of the Court. The Act provides three alternative methods for recovery of non-performing assets, namely: –

-The provisions of this Act apply to nonperforming assets (loans with an outstanding balance of more than Rs. 1 lakh) (NPA). This Act does not apply to NPA loan accounts that are less than 20% of the principal and interest.

-Recovery Methods Under the Act

The Act establishes three ways for recovering nonperforming assets (NPAs), including:

Securitization

Reconstruction of Assets

Enforcement of security without interrupting with the court

-Documents Required

e-Form CHG-1 or e-Form CHG-9 is required to be filed for application of a. Registration of creation b. Modification of charge (other than those related to debentures) including particulars of modification of charge by Asset Reconstruction Company in terms of Securitization and Reconstruction of Financial

-Assets and Enforcement of Securities Interest Act, 2002 [SARFAESI] The documents in this context are as follows:

Particulars of charge

Certificate of registration

An instrument created for the charge

Copy of the instrument – creating or modifying the charge

Hypothecation Deed

Sanction Letter

-In case of any e-Form to be digitally signed, either of the following is required:

DSC of the charge holder

Director Identification Number [DIN] of the Director

Permanent Account Number [PAN] of the manager, CEO, CFO

Membership Number of the Company Secretary

-Notification as amended up to June 30, 2015 - The Securitization Companies and Reconstruction Companies (Reserve Bank) Guidelines and Directions, 2003

https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=9901

The Guidelines for SCs/ARCs registered with the RBI are:

-Source RBI Website

https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=9901

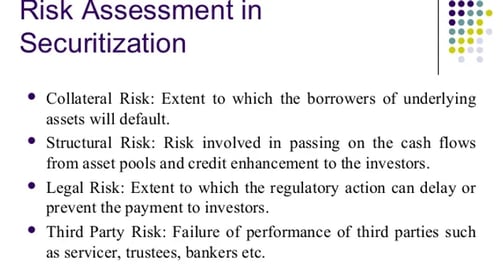

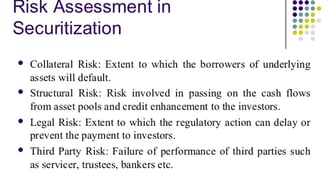

Risk Management in Securitization

-Legal risk is the risk of financial or reputational loss that can result from lack of awareness or misunderstanding of, ambiguity in, or reckless indifference to, the way law and regulation apply to your business, its relationships, processes, products, and services.

-Sovereign risk is the potential that a nation's government will default on its sovereign debt by failing to meet its interest or principal payments. Strong central banks can lower the perceived and actual riskiness of government debt, lowering the borrowing costs for those nations in turn.

-Prepayment risk of a fixed-income security's principal being returned early is referred to as prepayment risk. As a result, investors in related fixed-income securities will not be paid interest on their principal.

Information - For Reader.

Risk Management in Securitization

-Credit risk is a measurement of a borrower's creditworthiness. Lenders use credit risk to determine the chance of recovering all of their principal and interest when they make a loan. Borrowers with a low credit risk are subjected to reduced interest rates.

-Financial Guarantor Risk: An external agency may provide external credit protection in the form of insurance. Failure of a guarantor can have a negative impact on the stability of cash flows to investors.